Southeast Asia is an area of approximately 4.5 million square kilometres, roughly half the size of the United States. Countries that make up the region are:

- Maritime Southeast Asia: Indonesia, East Malaysia, Singapore, Philippines, East Timor and Brunei.

- Mainland Southeast Asia (known as Indochina): Cambodia, Laos, Myanmar (Burma), Thailand, Vietnam and West Malaysia.

In the 20th century, these countries have seen mixed fortunes in terms of economy and political upheavals, but overall the story has been one of rapid growth. Over the past decade, the region has averaged a growth rate of more than five percent per year. If Southeast Asia were one country, it would be the world's ninth-largest economy.

| State | Capital | Area (km2) | Population (2014) | GDP (nominal) USD million (2014) | GDP (nominal) per capita, USD (2014) |

|---|---|---|---|---|---|

| Brunei | Bandar Seri Begawan | 5,765 | 453,000 | 17,105 | $37,759 |

| Cambodia | Phnom Penh | 181,035 | 15,561,000 | 17,291 | $1,111 |

| East Timor | Dili | 14,874 | 1,172,000 | 4,382 | $3,739 |

| Indonesia | Jakarta | 1,904,569 | 251,490,000 | 1,187,962 | $4,723 |

| Laos | Vientiane | 236,800 | 6,557,000 | 11,206 | $1,709 |

| Malaysia | Kuala Lumpur* | 329,847 | 30,034,000 | 367,712 | $12,243 |

| Myanmar | Nay Pyi Daw | 676,000 | 51,419,000 | 63,881 | $964 |

| Philippines | Manila | 342,353 | 101,649,000 | 278,260 | $2,737 |

| Singapore | Singapore | 724 | 5,554,000 | 289,086 | $52,049 |

| Thailand | Bangkok | 513,120 | 65,236,000 | 437,344 | $6,703 |

| Vietnam | Hanoi | 331,210 | 92,571,000 | 187,848 | $2,072 |

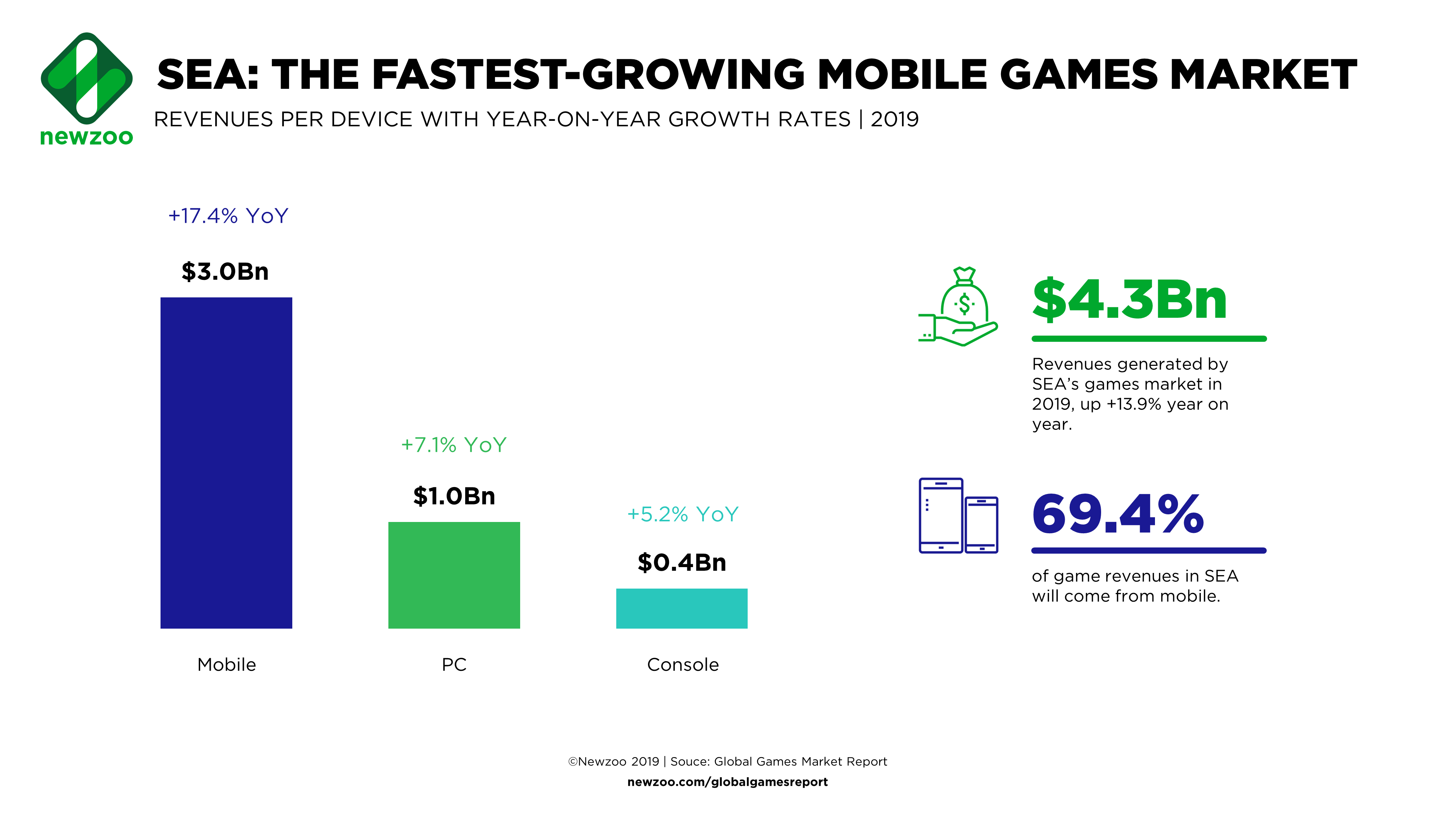

Until recently, the region was seen as playing catch-up with the developed world, but it’s now achieving a status of a significant market, including for mobile gaming. Southeast Asia’s economic growth prospects, huge population and fast-rising internet connectivity (especially mobile) all point towards solid growth in terms of game spending for many years to come. In addition, for a foreign company Southeast Asia is a region that could be easier to access than for instance China or Russia.

Southeast Asia is interesting for one other reason. Many Japanese, Korean and Chinese game companies have had mixed success in trying to conquer the West and have since shifted their attention to Southeast Asia which is closer in terms of geography and (game) culture. At the same time, Western companies have spotted the potential and set up local offices and localized content. Southeast Asia is gearing up to be a key battleground for mobile games, especially since the local market has not been divided up between homegrown players yet.

Why mobile gaming?

According to Newzoo, the global mobile market reached $77.2Bn in 2020, following impressive year-on-year growth rates of +15.8% and +2.7% for (smart)phones and tablets, respectively. Growth is expected to continue in the coming years.

.png?width=2871&name=Newzoo-2019-Global-Games-Market-per-Segment-1%20(edit).png)

The high mobile growth rate is driven by both organic growth, lifting the overall market, and cannibalistic growth, at the expense of other segments. In addition to the initial casualties of mobile growth (console, online casual and social gaming), Newzoo notes signs of slower growth in (online) browser PC games as spending is diverted to mobile devices.

Mobile games continue to grow in terms of players and revenue across all regions. An increase in the number of paying gamers and time spent gaming is fueling the Western markets while rising online connectivity, smartphone penetration and the availability of 4G connectivity drives rapid growth in emerging markets, such as Southeast Asia.

Mobile gaming in SEA

Mobile games strongly dominate across Southeast Asia. In 2020, the Asia-Pacific region (and by extension, Southeast Asia) was reported to have the highest smartphone ownership in the world, with 1,924Mn active users.

.png?width=3402&name=Newzoo_2019_Smartphone_Users_per_Region2%20(edit).png)

Global mobile games revenue has continued to rise, reaching $49Bn in 2019 and making up 60% of revenue for the overall gaming market. Southeast Asia alone has contributed a significant share to this growth, thanks in part to the fast-rising (mobile) internet connectivity across the region and its high population numbers.

Six countries in Southeast Asia make up the majority of the region’s mobile gaming market. The “Big 6” are Thailand, Vietnam, the Philippines, Malaysia, Singapore and Indonesia. These countries account for nearly 90% of the population of Southeast Asia. Much of the region’s population is young, with the majority in, or about to enter, the working age demographic. This plays a key role in the region’s current and forecast competitive advantage in the world economy.

.png?width=970&name=flags%20(part%201).png)

.png?width=970&name=flags%20(part%202).png)

Source: ©Newzoo

Revenues of the Southeast Asian games market are expected to continue increasing. Thailand will remain the largest market in terms of gaming revenues in Southeast Asia, closely followed by Indonesia and Malaysia. Singapore will continue to grow but will lose market share to faster growing countries. Vietnam and Thailand will grow in line with the overall market, maintaining their market share.

.png?width=2931&name=Newzoo-2020-Global-Gamers%20(edit).png)

Gaming itself is one of the most popular uses for mobile devices in the region. A Google survey indicated that over 1/3 of smartphone owners in each of the Big 6 Southeast Asian markets played mobile games at least once in the last seven days. The popularity of mobile gaming in the region is reflected in the iOS App Store and Google Play, especially when compared to South Korea, one the world’s largest and most influential app markets.

It is also worth noting that app store revenue is just a part of the overall mobile game opportunity in these countries. Publishers commonly use advertising and other indirect or subsidy-based monetization strategies to supplement the direct revenue that games generate from in-app purchases, paid downloads and in-app advertising. The split between IAP and advertising is growing ever wider toward advertising. Some publishers go as far as offering in-game currency in exchange for watching ads.

Like South Korea, Malaysia and Thailand are traditional Asian online PC game markets since the 2000s where people are much more used to paying for online games. Also, according to a series of studies conducted mid-decade by Euromonitor, annual disposable income and credit card penetration are higher in Malaysia and Thailand than in the other three markets. Both the willingness and ability to pay in Malaysia and Thailand might lead to better monetization of mobile games in these two countries.

Differences between countries

Over the past decade, differing economic conditions and telecommunication infrastructures played a key role in shaping personal computing device penetration and internet access in emerging Southeast Asian game markets. As a result, consumers developed different app- and phone-related behaviors and preferences.

It has been observed that less developed countries like Indonesia and Philippines have drawn less attention from app publishers. Fashion and trends in mobile gaming in these countries have been heavily influenced by Western markets, with inroads from China, Japan and South Korea.

In several Southeast Asian countries, universally popular mobile games from Western and Eastern developers continue to perform very well. However, unlike in Japan or South Korea, these games typically do not rely on large-scale TV and outdoor advertising campaigns to acquire users and downloads. Instead, it appears market growth is more organic. Gamers from Indonesia and the Philippines are reportedly reached through advertising automation channels such as Facebook, while in Vietnam, Thailand and Malaysia, better economic conditions and infrastructure enable higher penetration for PCs and internet access, which lay the foundation for online channels dedicated to discussions and downloads. Over the past decade, game companies from China, Japan and South Korea have entered these markets by establishing subsidiaries or licensing game products to local partners.

Indonesia and Thailand currently boast the largest percentage of payers – nearly 50% of players there spend money on mobile games. While Singapore has the lowest percentage of paying mobile gamers, in dollar terms they spend more than others per player.

Mobile messaging platforms and gaming

Messaging apps are expanding their ability to serve as gateways to new audiences for games and online services in China, Japan and South Korea (a trend that has been used to great effect in Southeast Asia).

Andovar’s client LINE is a market leader in the region. In Malaysia, Indonesia and Thailand, it took the #1 spot by revenue among apps outside of games and also ranked in the top 20 on the download charts. In Philippines and Vietnam, even though LINE didn’t rank in the top 10 by downloads, it still reached the top 10 by revenue. WeChat, which made significant progress in Malaysia, could be another major messaging app contender in the country. While there are other popular messaging apps in the region like Facebook Messenger, LINE was the only one that has successfully built a large game portfolio. However, in other SEA markets, messaging platforms are still in the earlier stage of their product lifecycle. Once they hit a critical level of users to capitalize on network effects, they could roll out games and services to their massive user bases.

Western messaging apps are also hoping to cash-in on this trend with popular apps such as Viber and Tango integrating games into their platforms. Tango, which received $215 million in investment from Alibaba in 2014, has over 250 million registered users and a huge selection of games, both in-house and externally made. According to the company, games on the Tango platform have 2-3x Life Time Value than that of the same games off platform. In the same year, Viber made its game service available to its 236 million monthly active users, following a successful two month pilot in five countries.

How does the region compare to others?

Witnessing the demand for mobile games, many PC and console game publishers from Asia swiftly pivoted to a mobile-first strategy. At the same time, the investor community continued to inject cash into the market and incubate companies vying for mobile dominance. Competition in the mobile game sector has never been fiercer in China, Japan and South Korea, motivating publishers to seek fresh opportunities.

Southeast Asia could become that next frontier and games are set to lead this growth, just as it has elsewhere, as Southeast Asia is growing faster than other emerging regions such as Latin America and Eastern Europe.

While China is a very attractive market also characterized by high growth and a huge population, Southeast Asia may be easier to enter for Western mobile publishers. The reasons behind this are lower competition, less regulation and widespread use of established Western distribution channels such as Google Play and iTunes App Store.

Half the top grossing games in Southeast Asia are Western titles. Western games are the most popular in the Philippines, where they make up 65% of the top games. Only 35% of the top games in Thailand are Western, the lowest percentage out of the Big 6. King and Supercell are by far the most dominant Western Publishers, with appearances in every Top 20 ranking.

Southeast Asia also shares many of the same preferences for social networks as the West. As high as 95% of those using mobile social networks or chat applications in Vietnam are actively on Facebook. The lowest percentage of Facebook users in the region is Indonesia, and that is still high at 78%.

Android or iOS?

In the five emerging Southeast Asian markets (Vietnam, Malaysia, Philippines, Thailand and Indonesia), Android holds a significant lead over iOS in device install base. The combination of lower purchasing power prevalent in the region and direct smartphone distribution favors the lower-priced Android devices.

In February 2015, Google released Android One devices in the Philippines and Indonesia. Android One is a set of smartphone standards designed for customers in developing countries primarily focused on people buying their first-ever smartphones. Android One smartphones run nearly stock Android with Google Mobile Services and can be built on reference hardware designs provided by Google. Google’s deeper involvement in software and hardware standards should reduce manufacturers’ R&D costs to help create more affordable phones, which is key to growing market share in emerging economies.

Over the last couple of years, Google Play ended up generating more than 4 times the mobile game downloads as the iOS App Store across the Big 6 Southeast Asian countries combined. The largest difference occurred in Indonesia, where Google Play was 9 times the size of iOS. The smallest difference was apparent in Vietnam, where Google Play was 3 times the size of iOS, though iOS maintained its lead position in game monetization and was 1.3 times as large as Google Play in the six markets combined. In Thailand, Vietnam, Indonesia and Philippines, the iOS App Store’s lead ranged from approximately 1.3 times to 2 times. Malaysia was the only country where Google Play’s revenue did not trail the iOS App Store’s.

The languages of Southeast Asia

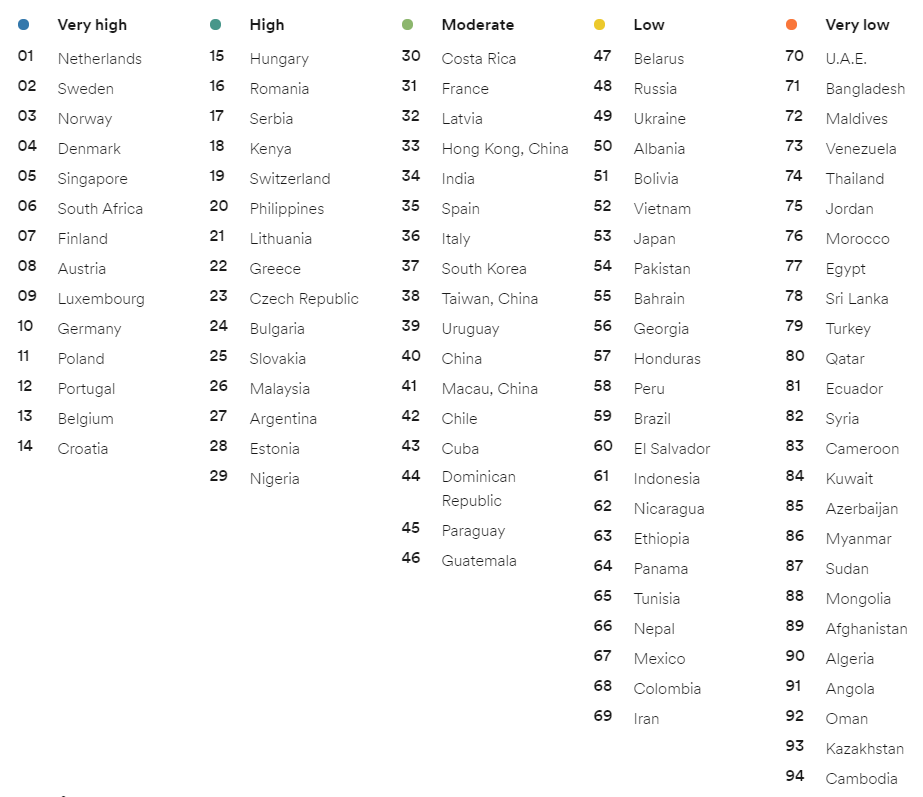

While all countries in the region are familiar with English as a language of international business and popular culture, actual fluency varies by country. In Singapore and the Philippines, English is an official second language. In Malaysia, English is an active second language, while other countries in Southeast Asia widely use English in business contexts. In China, on the other hand, English penetration is still less than 1%.

The below EF EPI English proficiency index by English First shows the differences clearly.

(5) Singapore, (20) the Philippines, (26) Malaysia, (52) Vietnam, (61) Indonesia, (74) Thailand

While many players in Malaysia and Singapore will be satisfied with English language versions of the game, the same cannot be said about the remaining countries. For example, Thailand is one of the largest and most promising markets, but is far behind its neighbors in the region when it comes to English proficiency. At the same time, localization into Thai is much more challenging than into established Western languages, or even Chinese or Japanese due to a complex writing system. The same can be said about Lao, Cambodian and Burmese, which all pose their own difficulties.

Summary

Mobile gaming has driven the growth of the global app economy. We believe Southeast Asia is especially interesting to enter now for the following reasons:

- Games are already the largest mobile app category in emerging Southeast Asia and are growing at a staggering rate.

- Mobile games have experienced surprising growth in Southeast Asia, with some countries showing game revenue growth of over 100%.

- There are still blue-ocean markets in the region with entertainment-hungry populations ready to consume the next hit game, and ripe opportunities for game distribution platforms.

- Southeast Asian markets are easier to enter for international publishers than other emerging countries, like Russia or China.

Sources: Free reports published by AppAnnie and Newzoo.

The Andovar advantage

If you're looking for advice on entering the international gaming market, whether in Southeast Asia or elsewhere, feel free to get in touch with us here at Andovar.

Our offices are located in Singapore (global headquarters), India, China, Thailand, Hungary and Colombia. We provide customized localization solutions for even the most complex of gaming projects. Our turnkey localization services include localization engineering, voice localization (including voice-over dubbing and/or subtitling), text localization, integration and a complete range of testing options.

For those interested in learning more about the game localization process itself, please feel free to check out our Ultimate Games Translation Guide.